July 30, 2025

Wave riding in fintech

By Adams Conrad and Amias Gerety

It will be years before we see meaningful revenue from AI-focused fintechs.

Here’s a thought experiment: what would have happened if the Collison brothers, who founded the fintech giant Stripe, had focused on enabling payments for newspapers? I have no reason to doubt that the Collisons are the defining archetype of “generational” founders, but who believes that Stripe could have been one-tenth the company that it is if it had focused on other sectors?

Finance is downstream of the real economy. Fintech 1.0 (e.g. Lending Club, SoFi and Credit Karma) was a straightforward outgrowth of technology, enabling lending over the internet and on people’s phones. Moreover, Fintech 1.0 was driven by the great financial crisis and a multi-year pullback by banks from the business of innovation and customer service as they licked their wounds, repaired their balance sheets and got serious about risk and compliance.

Fintech 2.0 (think Robinhood, Chime) was powered by an even further consolidation of financial services onto the phone, combined with a series of clever business model arbitrages that were differentially dedicated to serving up financial services in much smaller increments.

For example, Chime is powered by a debit interchange rate that is simply not available to banks above $10 billion, or anywhere else in the world for that matter. Current, one of our portfolio companies, recognized that enabling customers to access their paychecks on the day the paycheck is sent, rather than waiting the typical two-day settlement period, was among the most valuable credit features they could offer. Robinhood wouldn’t have been possible without the ability to purchase fractional shares and the insight that large hedge funds and market makers would actually pay them for the privilege of knowing that their counterparty wasn’t another massive financial institution.

Perhaps just as importantly, the most successful companies in Fintech 2.0 rode the COVID wave perfectly. COVID pulled forward about a decade’s worth of digital adoption in finance, while giving working-class Americans extra cash and forced “downtime,” two huge macro trends that powered these companies from successful startups to household names.

It’s an uncomfortable truth for fintech investors that our companies facilitate new forms of economic activity, but those of us in financial services don’t create new forms of economic activity. Home runs in fintech investing ride larger forces in the economy. But just like in surfing, if you try to catch a wave before it’s ready to break, you can’t possibly paddle fast enough to catch it. Experienced surfers know that each beach has its own take-off zone where you need to be to catch the big ones.

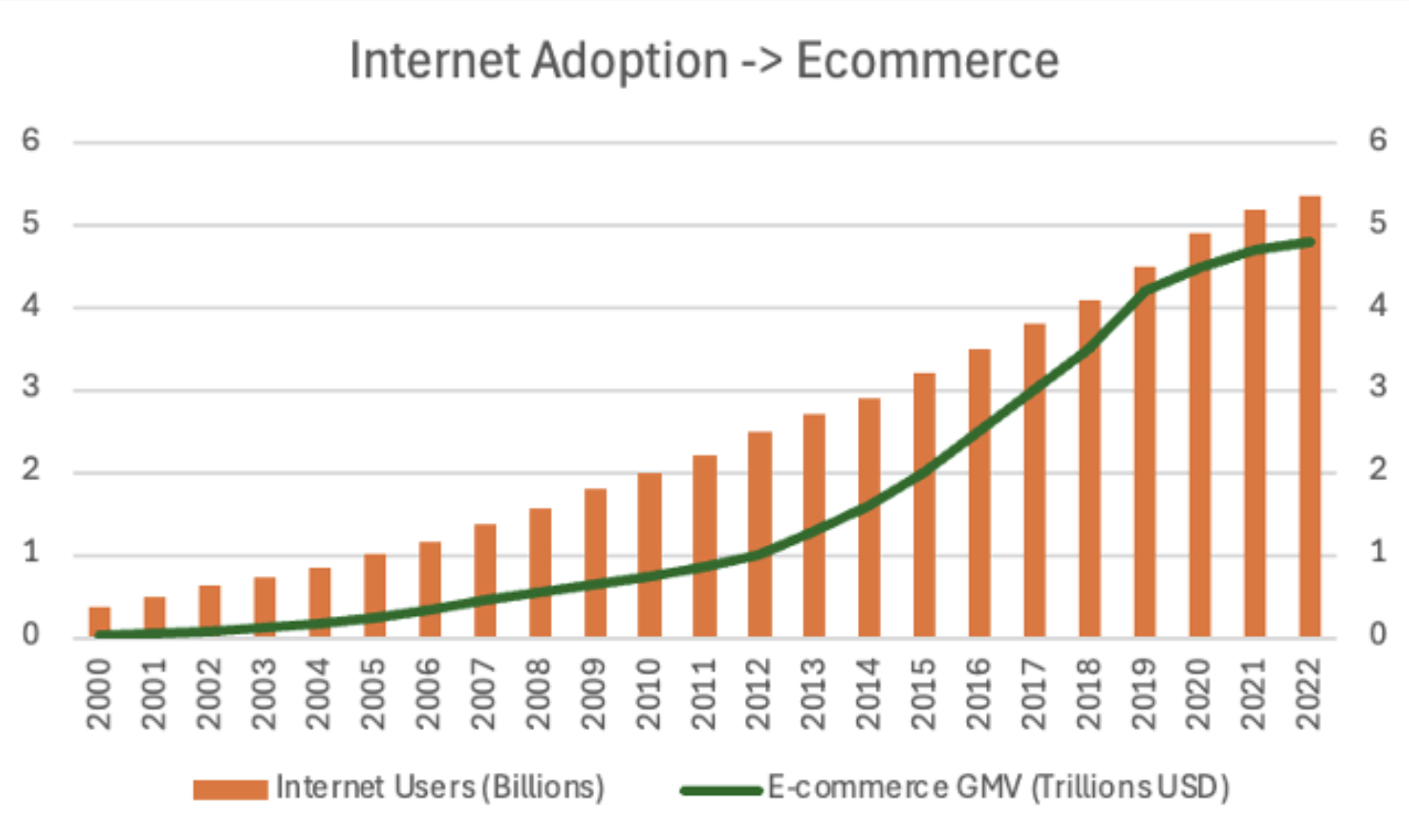

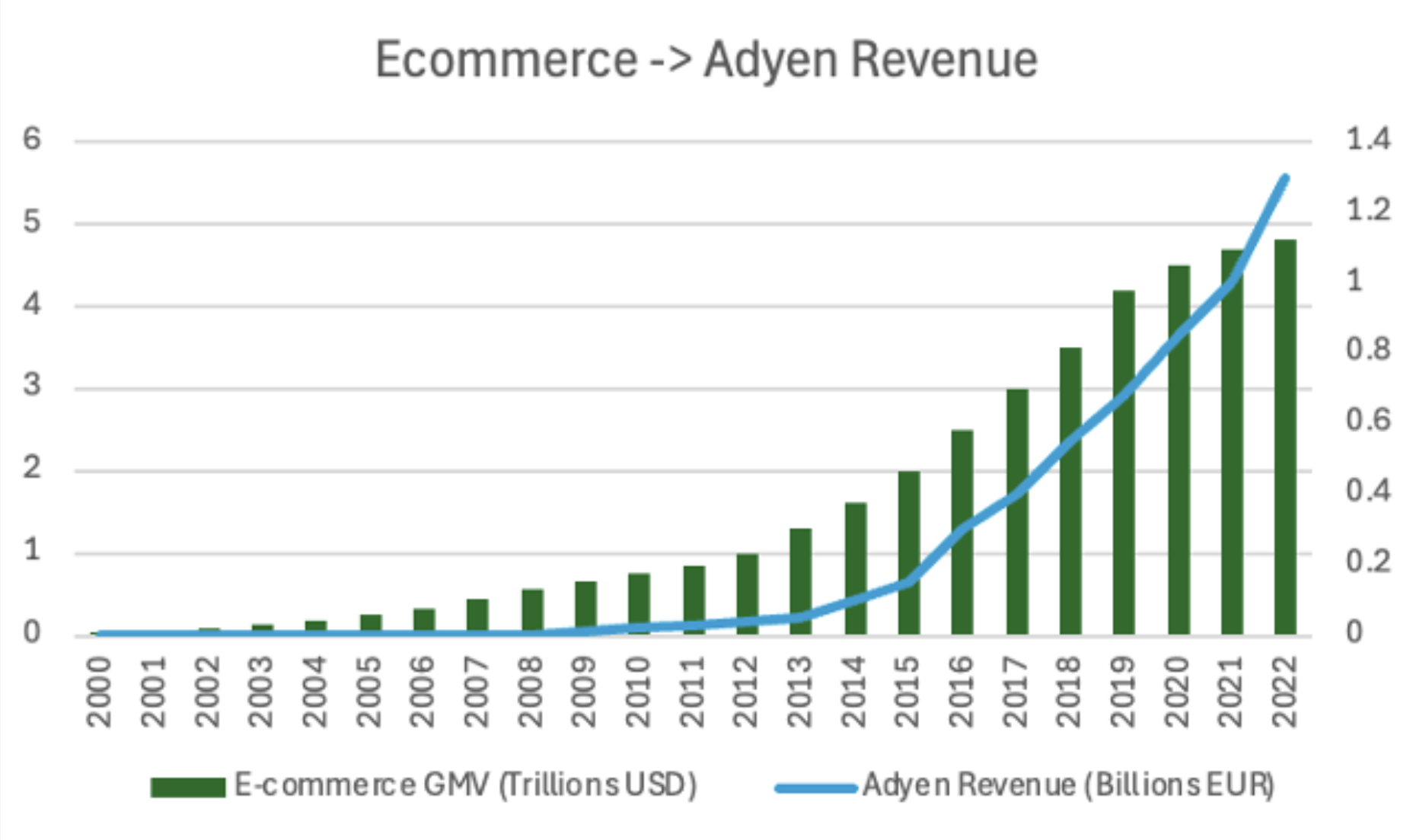

Back to Stripe and Adyen, these companies are two of the largest fintechs and have done so by facilitating the economy of the internet. But amazingly, despite the tailwinds, the internet took 10 years AFTER the dot-com crash to generate $1 trillion in e-commerce spending. Adyen took another decade after that to generate $1 billion of annual revenue.

Internet adoption has been the most important economic trend of our lifetime. It has conquered the world with 5 billion users globally. Still, the trend is basically linear – a 22-year compound annual growth rate of 13 percent. E-commerce got a much slower start – still close to zero even during the dot-com boom – but has grown even more explosively. The 22-year growth rate for items purchased on the internet has been twice as fast at 26 percent.

What happened to Adyen is even more remarkable.

Even compared to e-commerce volume, Adyen’s revenue growth is explosive. Adyen’s revenue has grown three times faster than the underlying e-commerce volume trend, with a compound annual growth rate of over 70 percent per year.

It’s not yet obvious that AI is more important than the internet. But it is clear that it is the most important technological factor driving the world economy today. (Sorry crypto!)

Everyone is rushing to participate in the gold rush and ‘wise’ VCs like us are naturally excited to invest in the fintech companies that will facilitate this economic transformation. Everyone knows that you make money by investing in picks and shovels. But our sense is that early stage investors will likely need patience in their approach to artificial intelligence.

From a fintech perspective, the growth of OpenAI, Claude, Gemini will act like internet adoption. The growth of these LLMs, along with other emerging juggernauts like Cursor, Lovable, and Bolt and a wave of decentralized data center investment, are laying the infrastructure for new kinds of economic activity that will require new kinds of financial services.

It’s certainly possible that AI will move more quickly than previous cycles. Generative AI has generated the fastest-growing software companies in history. Similarly, in the application layer, AI-marketing, AI-outbound and AI-voice agents have experienced incredibly rapid adoption.

Across our portfolios, the mantra is: ‘AI isn’t perfect, but user acceptance is way higher than you might fear.’ We repeatedly see that customer satisfaction is higher after interacting with an AI agent, and often key KPIs like conversion are higher as well.

But for fintech, we’re simultaneously all-in and counseling patience. We’re constantly encouraging our companies to do more experiments and adopt AI and agents more aggressively. We’re also biding our time on investing in AI-specific infrastructure companies.

In fintech, a first-mover advantage more often looks like a disadvantage. As we've written in the “inverted AI” thesis, the world isn’t ready for the world that AI is building. We still don’t really know which financial pathways are necessary or which ones will slingshot as they unlock new economic opportunities.

Finally, the very ease of consumer adoption (AI is software that almost sells itself) means that competition will be even more fierce and it may take more time for execution advantages to be revealed.

By Adams Conrad and Amias Gerety

It will be years before we see meaningful revenue from AI-focused fintechs.

Here’s a thought experiment: what would have happened if the Collison brothers, who founded the fintech giant Stripe, had focused on enabling payments for newspapers? I have no reason to doubt that the Collisons are the defining archetype of “generational” founders, but who believes that Stripe could have been one-tenth the company that it is if it had focused on other sectors?

Finance is downstream of the real economy. Fintech 1.0 (e.g. Lending Club, SoFi and Credit Karma) was a straightforward outgrowth of technology, enabling lending over the internet and on people’s phones. Moreover, Fintech 1.0 was driven by the great financial crisis and a multi-year pullback by banks from the business of innovation and customer service as they licked their wounds, repaired their balance sheets and got serious about risk and compliance.

Fintech 2.0 (think Robinhood, Chime) was powered by an even further consolidation of financial services onto the phone, combined with a series of clever business model arbitrages that were differentially dedicated to serving up financial services in much smaller increments.

For example, Chime is powered by a debit interchange rate that is simply not available to banks above $10 billion, or anywhere else in the world for that matter. Current, one of our portfolio companies, recognized that enabling customers to access their paychecks on the day the paycheck is sent, rather than waiting the typical two-day settlement period, was among the most valuable credit features they could offer. Robinhood wouldn’t have been possible without the ability to purchase fractional shares and the insight that large hedge funds and market makers would actually pay them for the privilege of knowing that their counterparty wasn’t another massive financial institution.

Perhaps just as importantly, the most successful companies in Fintech 2.0 rode the COVID wave perfectly. COVID pulled forward about a decade’s worth of digital adoption in finance, while giving working-class Americans extra cash and forced “downtime,” two huge macro trends that powered these companies from successful startups to household names.

It’s an uncomfortable truth for fintech investors that our companies facilitate new forms of economic activity, but those of us in financial services don’t create new forms of economic activity. Home runs in fintech investing ride larger forces in the economy. But just like in surfing, if you try to catch a wave before it’s ready to break, you can’t possibly paddle fast enough to catch it. Experienced surfers know that each beach has its own take-off zone where you need to be to catch the big ones.

Back to Stripe and Adyen, these companies are two of the largest fintechs and have done so by facilitating the economy of the internet. But amazingly, despite the tailwinds, the internet took 10 years AFTER the dot-com crash to generate $1 trillion in e-commerce spending. Adyen took another decade after that to generate $1 billion of annual revenue.

Internet adoption has been the most important economic trend of our lifetime. It has conquered the world with 5 billion users globally. Still, the trend is basically linear – a 22-year compound annual growth rate of 13 percent. E-commerce got a much slower start – still close to zero even during the dot-com boom – but has grown even more explosively. The 22-year growth rate for items purchased on the internet has been twice as fast at 26 percent.

What happened to Adyen is even more remarkable.

Even compared to e-commerce volume, Adyen’s revenue growth is explosive. Adyen’s revenue has grown three times faster than the underlying e-commerce volume trend, with a compound annual growth rate of over 70 percent per year.

It’s not yet obvious that AI is more important than the internet. But it is clear that it is the most important technological factor driving the world economy today. (Sorry crypto!)

Everyone is rushing to participate in the gold rush and ‘wise’ VCs like us are naturally excited to invest in the fintech companies that will facilitate this economic transformation. Everyone knows that you make money by investing in picks and shovels. But our sense is that early stage investors will likely need patience in their approach to artificial intelligence.

From a fintech perspective, the growth of OpenAI, Claude, Gemini will act like internet adoption. The growth of these LLMs, along with other emerging juggernauts like Cursor, Lovable, and Bolt and a wave of decentralized data center investment, are laying the infrastructure for new kinds of economic activity that will require new kinds of financial services.

It’s certainly possible that AI will move more quickly than previous cycles. Generative AI has generated the fastest-growing software companies in history. Similarly, in the application layer, AI-marketing, AI-outbound and AI-voice agents have experienced incredibly rapid adoption.

Across our portfolios, the mantra is: ‘AI isn’t perfect, but user acceptance is way higher than you might fear.’ We repeatedly see that customer satisfaction is higher after interacting with an AI agent, and often key KPIs like conversion are higher as well.

But for fintech, we’re simultaneously all-in and counseling patience. We’re constantly encouraging our companies to do more experiments and adopt AI and agents more aggressively. We’re also biding our time on investing in AI-specific infrastructure companies.

In fintech, a first-mover advantage more often looks like a disadvantage. As we've written in the “inverted AI” thesis, the world isn’t ready for the world that AI is building. We still don’t really know which financial pathways are necessary or which ones will slingshot as they unlock new economic opportunities.

Finally, the very ease of consumer adoption (AI is software that almost sells itself) means that competition will be even more fierce and it may take more time for execution advantages to be revealed.