July 31, 2025

July 2025 newsletter: IPO market, pipeline trends and fintech themes

Message from Nigel Morris, Managing Partner:

At the start of 2025, expectations for a revitalized IPO market were high. After several lean years following the 2021 IPO frenzy, when 61 fintechs went public compared to just 18 over the next three years, investors were hungry for liquidity. A growing group of mature, profitable fintechs seemed poised to answer the call.

Our third annual global fintech report, with our friends at Boston Consulting Group, Fintech’s Next Chapter: Scaled Winners and Emerging Disruptors, showed that fintech fundamentals significantly strengthened in 2024. Global revenues among fintechs grew by a robust 21 percent year-over-year (compared to 13 percent in 2023), well ahead of the six percent growth in the broader financial services industry. Further, fintech is only three percent penetrated, representing about $380 billion of the $14.5 trillion revenue base for financial services worldwide.

However, despite strengthening fintech fundamentals, macroeconomic volatility, tariffs and ongoing uncertainty abruptly delayed IPO ambitions, with companies like Klarna choosing to put their IPO plans on hold for the moment.

That brief pause has given way to an IPO market resembling something closer to the environment of 2018 or 2019. In recent months, fintechs like eToro (public as of May 14), Chime (profitable and disciplined in the run-up to IPO) and Circle (whose stock is up more than 500 percent since its debut) have all made successful entries into the public markets.

Our research shows this renewed momentum could trigger a powerful flywheel of capital recycling into private markets. This resurgence will help propel the fintech ecosystem forward, with earlier-stage fintechs poised to benefit from the $677 billion in venture capital dry powder available globally. And nearly 400 fintechs have reached unicorn status.

All of the IPOs hitting the market now have been years in the making. As the doors open and confidence builds, we believe the stream will grow stronger, especially as fintechs continue to shift from a “growth at all costs” mindset to a “profitable growth” philosophy.

The successful debut of these companies is likely to inspire others who have been waiting on the sidelines due to timing or market concerns. As highlighted in our global report, the fintech industry is structurally positioned for a resurgence, with conditions aligning for a new wave of IPOs. One signal of what's ahead is the fact that there are 150 fintechs founded before 2016 that have each raised over $500 million in equity and have yet to go public, including some of the sector’s most recognized names like Stripe, Revolut, Monzo and Klarna.

In anticipation of going public, we convened our CEOs in NYC in February for an IPO readiness seminar. We hosted 16 of our portfolio companies that could be IPO candidates over the next two to three years to explore the strategic and operational complexities a CEO must take into account when considering taking their company public.

Looking ahead, a few things to watch out for:

- Fintech IPOs will continue, but at a steady pace. Both companies and investors are being selective.

- M&A will accelerate. Some companies may not have a viable IPO path and will consolidate to grow or survive.

- The continued return of "surefooted growth". Investors are still rewarding growth, but only when paired with sound unit economics and financial discipline.

We're optimistic about what this shift signals for the sector. Fintech innovation has not slowed. If anything, it has matured. Now, the markets are finally catching up.

For more on where fintech is headed, I shared my perspective on changes to the CFPB, late fees, bank charters and more in recent TV interviews with Squawk Box Europe, Nasdaq and Yahoo Finance.

+++

Let's connect:

I'll be heading to Brazil next week, D.C. for the CEO Summit in September, speaking at the Tom Brown Second Curve Capital conference in Chicago this October and in Mexico City in November. Please reach out if you'd like to connect.

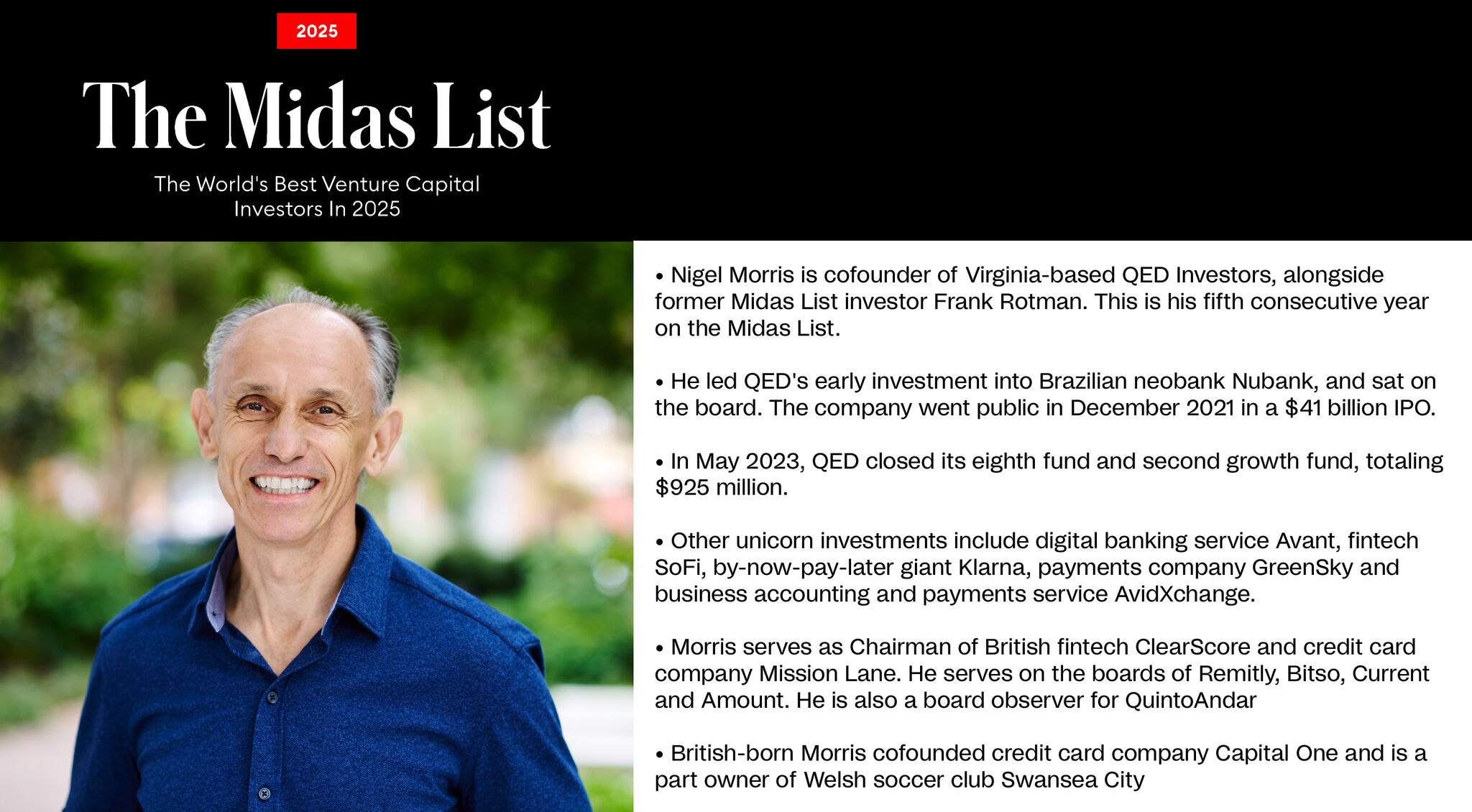

For the fifth year in a row, Nigel has been named to Forbes’ annual Midas List highlighting the best venture capitalists in the world. He ranked No. 90 on the 2025 list.

At least one member of the QED team has been recognized on Forbes’ list every year since 2018.

Trends We're Tracking

Artificial intelligence

Artificial Intelligence is everywhere. We started investing in fintech over 17 years ago. While we’ve seen a few different waves drive innovation in the industry, this wave is as big as any. Fintechs are incredibly well-positioned for AI adoption, growing three times faster than incumbents as they leverage digital distribution channels and increasingly utilize AI to slash costs in labor-intensive areas, aid in cost improvements and drive mass customization. Startups will continue to leverage GenAI to reinvent themselves, unleashing the next wave of fintechs that will be hyper-data-driven, personalized powerhouses loved by the customers they serve. There remains an incredible opportunity for financial services companies, but also a lot to learn.

Read our thoughts on AI agents and the future of agentic payments.

Stablecoins globally

Stablecoins are a compelling use case for blockchain technology, offering programmable, 24/7, dollar-based transactions that can improve the speed, cost and accessibility of cross-border payments—especially in underbanked markets. While today’s applications are often niche or speculative, we see long-term potential in enterprise-grade, compliant solutions that augment rather than replace the existing financial system. Our investment focus is on infrastructure and use cases that prioritize trust, transparency and integration with mainstream finance—not speculative tokens, exchanges or crypto-native apps with diminishing differentiation. We believe institutions that understand compliance and control will shape the next wave of adoption, strengthening U.S. financial leadership in the process.

Latin America and the energy sector

The energy sector is one of Latin America’s largest and most antiquated industries. Despite partial liberalization in markets like Brazil and Mexico, most incumbents operate with little differentiation, and consumers often don’t realize they have a choice in energy retailers. Many still receive opaque, physical bills they don’t understand and pay them without question. This creates fertile ground for disruption through technology, transparency and a better customer experience.

We see significant opportunities at the intersection of energy, data and fintech. Real-time data can unlock smarter consumption, improve grid efficiency and support the decarbonization agenda. Fintech layers, such as embedded billing, credit underwriting tied to energy usage or BNPL for distributed solar, can radically improve customer acquisition and retention while solving structural working capital pain points for installers and retailers.

What’s often overlooked is the complexity of building in this sector: regulatory hurdles, hardware dependencies, capex-heavy cycles and long sales motions. To unlock this opportunity, venture capitalists will need to rethink their frameworks, adjusting time horizons, structuring capital creatively and helping founders navigate policy and infrastructure constraints. At QED, we’ve leaned into these challenges and partnered with founders shaping the future of energy in LatAm, where fintech infrastructure, energy transition and consumer empowerment converge.

Pipeline Trends

Analyzing the trends

Cole Lundquist, principal at QED, analyzed insights from QED’s second quarter pipeline. The data showed that, in the U.S. and Latin America, 20 percent of the pipeline from the second quarter was some combination of AI, stablecoins and agentic payments. This is the largest category of deal flow by a factor of 2.5x and it absolutely reflects the current sentiment in fintech investing. Stablecoins are the first global mass adoption use case for blockchain technology and specialists and generalists alike are piling into deals. We are seeing valuations run wild in these three segments as well.

Want to learn more? Connect with Cole Lundquist.

Where We've Been

SuperReturn International

QED partner and head of early stage investments Bill Cilluffo, QED partner and head of global capital strategy Fernando Gonzalez, and Katherine Tercek, QED's head of investor relations, headed to Berlin for SuperReturn International. During the event, they met with current and prospective LPs as well as friends from the ecosystem.Listen to Bill's interview with Emma Walden.

Brazil at Silicon Valley Conference

Camila Vieira Fernandes, partner and head of Brazil, took the stage at the BSV conference to discuss adapting venture capital strategies for Latin America.

.JPG)

New York Tech Week

The launch of the third edition of our global fintech report in partnership with Boston Consulting Group: Fintech’s Next Chapter: Scaled Winners and Emerging Disruptors took place during Tech Week in NYC.

The evening featured a wonderful panel on the state of fintech, moderated by Nik Milanović from This Week in Fintech, with CEOs Gal Krubiner from Pagaya, Stuart Sopp from Current, and Daniel Vogel from Bitso.

Read the report here.

Web Summit Rio

QED partner and head of LatAm, Mike Packer, joined The J Curve with host Olga Maslikhova live from Web Summit Rio to discuss how we built conviction that the LatAm market was big enough and the founder quality strong enough to justify a dedicated strategy more than a decade ago.Mike shares why you can’t shortcut fundamentals when building companies, where real-time payments will expand across the region and how stablecoins are starting to show up in real-world transactions.Listen to the podcast here.

We hosted a fantastic meetup in India with over 100 attendees across banking, PE/VC, operators and founders. We capped the evening with an exceptional dinner and great company. It was a pleasure to share a meal and some laughs with the leadership from India portcos.

Message from Nigel Morris, Managing Partner:

At the start of 2025, expectations for a revitalized IPO market were high. After several lean years following the 2021 IPO frenzy, when 61 fintechs went public compared to just 18 over the next three years, investors were hungry for liquidity. A growing group of mature, profitable fintechs seemed poised to answer the call.

Our third annual global fintech report, with our friends at Boston Consulting Group, Fintech’s Next Chapter: Scaled Winners and Emerging Disruptors, showed that fintech fundamentals significantly strengthened in 2024. Global revenues among fintechs grew by a robust 21 percent year-over-year (compared to 13 percent in 2023), well ahead of the six percent growth in the broader financial services industry. Further, fintech is only three percent penetrated, representing about $380 billion of the $14.5 trillion revenue base for financial services worldwide.

However, despite strengthening fintech fundamentals, macroeconomic volatility, tariffs and ongoing uncertainty abruptly delayed IPO ambitions, with companies like Klarna choosing to put their IPO plans on hold for the moment.

That brief pause has given way to an IPO market resembling something closer to the environment of 2018 or 2019. In recent months, fintechs like eToro (public as of May 14), Chime (profitable and disciplined in the run-up to IPO) and Circle (whose stock is up more than 500 percent since its debut) have all made successful entries into the public markets.

Our research shows this renewed momentum could trigger a powerful flywheel of capital recycling into private markets. This resurgence will help propel the fintech ecosystem forward, with earlier-stage fintechs poised to benefit from the $677 billion in venture capital dry powder available globally. And nearly 400 fintechs have reached unicorn status.

All of the IPOs hitting the market now have been years in the making. As the doors open and confidence builds, we believe the stream will grow stronger, especially as fintechs continue to shift from a “growth at all costs” mindset to a “profitable growth” philosophy.

The successful debut of these companies is likely to inspire others who have been waiting on the sidelines due to timing or market concerns. As highlighted in our global report, the fintech industry is structurally positioned for a resurgence, with conditions aligning for a new wave of IPOs. One signal of what's ahead is the fact that there are 150 fintechs founded before 2016 that have each raised over $500 million in equity and have yet to go public, including some of the sector’s most recognized names like Stripe, Revolut, Monzo and Klarna.

In anticipation of going public, we convened our CEOs in NYC in February for an IPO readiness seminar. We hosted 16 of our portfolio companies that could be IPO candidates over the next two to three years to explore the strategic and operational complexities a CEO must take into account when considering taking their company public.

Looking ahead, a few things to watch out for:

- Fintech IPOs will continue, but at a steady pace. Both companies and investors are being selective.

- M&A will accelerate. Some companies may not have a viable IPO path and will consolidate to grow or survive.

- The continued return of "surefooted growth". Investors are still rewarding growth, but only when paired with sound unit economics and financial discipline.

We're optimistic about what this shift signals for the sector. Fintech innovation has not slowed. If anything, it has matured. Now, the markets are finally catching up.

For more on where fintech is headed, I shared my perspective on changes to the CFPB, late fees, bank charters and more in recent TV interviews with Squawk Box Europe, Nasdaq and Yahoo Finance.

+++

Let's connect:

I'll be heading to Brazil next week, D.C. for the CEO Summit in September, speaking at the Tom Brown Second Curve Capital conference in Chicago this October and in Mexico City in November. Please reach out if you'd like to connect.

For the fifth year in a row, Nigel has been named to Forbes’ annual Midas List highlighting the best venture capitalists in the world. He ranked No. 90 on the 2025 list.

At least one member of the QED team has been recognized on Forbes’ list every year since 2018.

Trends We're Tracking

Artificial intelligence

Artificial Intelligence is everywhere. We started investing in fintech over 17 years ago. While we’ve seen a few different waves drive innovation in the industry, this wave is as big as any. Fintechs are incredibly well-positioned for AI adoption, growing three times faster than incumbents as they leverage digital distribution channels and increasingly utilize AI to slash costs in labor-intensive areas, aid in cost improvements and drive mass customization. Startups will continue to leverage GenAI to reinvent themselves, unleashing the next wave of fintechs that will be hyper-data-driven, personalized powerhouses loved by the customers they serve. There remains an incredible opportunity for financial services companies, but also a lot to learn.

Read our thoughts on AI agents and the future of agentic payments.

Stablecoins globally

Stablecoins are a compelling use case for blockchain technology, offering programmable, 24/7, dollar-based transactions that can improve the speed, cost and accessibility of cross-border payments—especially in underbanked markets. While today’s applications are often niche or speculative, we see long-term potential in enterprise-grade, compliant solutions that augment rather than replace the existing financial system. Our investment focus is on infrastructure and use cases that prioritize trust, transparency and integration with mainstream finance—not speculative tokens, exchanges or crypto-native apps with diminishing differentiation. We believe institutions that understand compliance and control will shape the next wave of adoption, strengthening U.S. financial leadership in the process.

Latin America and the energy sector

The energy sector is one of Latin America’s largest and most antiquated industries. Despite partial liberalization in markets like Brazil and Mexico, most incumbents operate with little differentiation, and consumers often don’t realize they have a choice in energy retailers. Many still receive opaque, physical bills they don’t understand and pay them without question. This creates fertile ground for disruption through technology, transparency and a better customer experience.

We see significant opportunities at the intersection of energy, data and fintech. Real-time data can unlock smarter consumption, improve grid efficiency and support the decarbonization agenda. Fintech layers, such as embedded billing, credit underwriting tied to energy usage or BNPL for distributed solar, can radically improve customer acquisition and retention while solving structural working capital pain points for installers and retailers.

What’s often overlooked is the complexity of building in this sector: regulatory hurdles, hardware dependencies, capex-heavy cycles and long sales motions. To unlock this opportunity, venture capitalists will need to rethink their frameworks, adjusting time horizons, structuring capital creatively and helping founders navigate policy and infrastructure constraints. At QED, we’ve leaned into these challenges and partnered with founders shaping the future of energy in LatAm, where fintech infrastructure, energy transition and consumer empowerment converge.

Pipeline Trends

Analyzing the trends

Cole Lundquist, principal at QED, analyzed insights from QED’s second quarter pipeline. The data showed that, in the U.S. and Latin America, 20 percent of the pipeline from the second quarter was some combination of AI, stablecoins and agentic payments. This is the largest category of deal flow by a factor of 2.5x and it absolutely reflects the current sentiment in fintech investing. Stablecoins are the first global mass adoption use case for blockchain technology and specialists and generalists alike are piling into deals. We are seeing valuations run wild in these three segments as well.

Want to learn more? Connect with Cole Lundquist.

Where We've Been

SuperReturn International

QED partner and head of early stage investments Bill Cilluffo, QED partner and head of global capital strategy Fernando Gonzalez, and Katherine Tercek, QED's head of investor relations, headed to Berlin for SuperReturn International. During the event, they met with current and prospective LPs as well as friends from the ecosystem.Listen to Bill's interview with Emma Walden.

Brazil at Silicon Valley Conference

Camila Vieira Fernandes, partner and head of Brazil, took the stage at the BSV conference to discuss adapting venture capital strategies for Latin America.

New York Tech Week

The launch of the third edition of our global fintech report in partnership with Boston Consulting Group: Fintech’s Next Chapter: Scaled Winners and Emerging Disruptors took place during Tech Week in NYC.

The evening featured a wonderful panel on the state of fintech, moderated by Nik Milanović from This Week in Fintech, with CEOs Gal Krubiner from Pagaya, Stuart Sopp from Current, and Daniel Vogel from Bitso.

Read the report here.

Web Summit Rio

QED partner and head of LatAm, Mike Packer, joined The J Curve with host Olga Maslikhova live from Web Summit Rio to discuss how we built conviction that the LatAm market was big enough and the founder quality strong enough to justify a dedicated strategy more than a decade ago.Mike shares why you can’t shortcut fundamentals when building companies, where real-time payments will expand across the region and how stablecoins are starting to show up in real-world transactions.Listen to the podcast here.

We hosted a fantastic meetup in India with over 100 attendees across banking, PE/VC, operators and founders. We capped the evening with an exceptional dinner and great company. It was a pleasure to share a meal and some laughs with the leadership from India portcos.